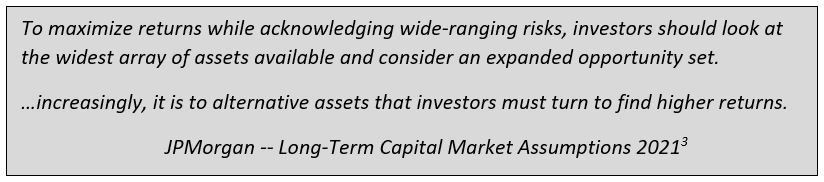

We believe asset allocation and a disciplined evaluation of risk and return are hallmarks of an effective investment process and critical within the current environment. Read how adding a diversified sleeve of alternative investments to investors’ portfolios can reduce expected volatility and increase expected returns.

by Matt Brunini Leave a Comment